This is the first in a series of articles designed to help the more technical people understand the business. They are intended as general reference material. A copy of the second article, Basics of Accounting: Closing the Books, can be found here.

The general ledger (GL) is the repository and reporting vehicle for all financial subledger transactions. Subledgers include the Oracle® Applications modules such as: Accounts Payable (AP), Accounts Receivable (AR), Order Management (OE), Human Resources (HR), Inventory (INV), etc.

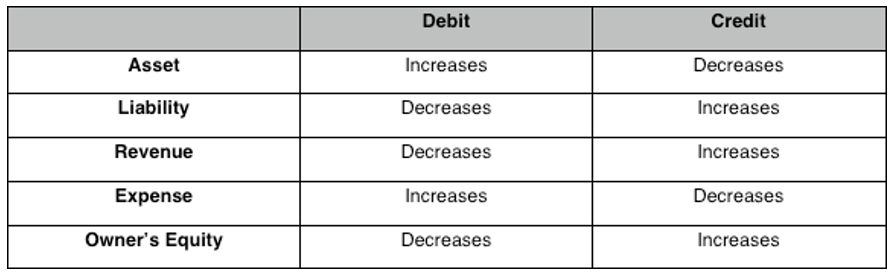

A general ledger stores a transaction as either a debit or a credit. Debits and credits perform different functions depending on the account types of the different transactions. There are five account types that are set up in Oracle Applications for the natural account segment of the accounting flexfield:

Asset: Assets are things of value used by a business and its operations and are usually classified as either tangible (cash, receivables, land, etc.) or intangible (patents, copyrights, and other nonphysical rights). A debit increases assets, while a credit decreases assets.

Liability: Liabilities are existing debts and obligations such as wages payable, mortgage taxes payable, and real estate taxes payable. Such obligations are generally termed accounts payable. A debit decreases liabilities, while a credit increases liabilities.

Revenue: Revenues are cash or other asset inflows to the business. However, revenues may take the form of a decrease in a liability as well as the increase in an asset. Sales, services, and royalties are examples of common forms of revenue. A debit decreases revenue, while a credit increases revenue.

Expense: Expense is the cost of assets consumed or services used in the process of earning revenue, and they can represent actual or expected outflows. Common expense accounts include wages, rent, and interest expense. A debit increase expenses, while a credit increases expenses.

Owner’s Equity: Owner’s equity is equal to total assets minus total liabilities. When an investment is made in a business, capital and owner’s equity are increased. If an owner withdraws money from a business, total owner’s equity is decreased. A debit decreases owner’s equity, while a credit increases owner’s equity.

These accounts can be classified within 3 types of General Ledger Accounts:

Balance Sheet Accounts: Assets, liabilities and owner’s equities are referred to as balance sheet accounts since the balances in these accounts are reported on the financial statement known as the balance sheet. The balance sheet accounts are also known as permanent accounts (or real accounts) since the balances in these accounts will not be closed at the end of an accounting year. Instead, these account balances are carried forward to the next accounting year.

Income Statement Accounts: Revenue and expense are referred to as income statement accounts since the amounts in these accounts will be reported on the financial statement known as the income statement. The income statement accounts are also known as temporary accounts since the balances in these accounts will be closed at the end of the accounting year. Each income statement account is closed in order to begin the next accounting year with a zero balance.

Chart of Accounts: The chart of accounts is simply a list of all of the accounts that are available for recording transactions. This means that the number of accounts in the chart of accounts will be greater than the number of accounts in the general ledger. The chart of accounts is organized similar to the general ledger: balance sheet accounts followed by the income statement accounts. However, the chart of accounts does not contain any entries or account balances. The chart of accounts allows you to find the name of an account, its account number and a brief description. It is important to expand and/or alter the chart of accounts to accommodate the changes to an organization and when there is a need for improved reporting of information. The chart of accounts is also used to designate where an account will be reported in the financial statements.